Today we’ll look at Creative Peripherals and Distribution Limited (NSE:CREATIVE) and reflect on its potential as an investment. In particular, we’ll consider its Return On Capital Employed (ROCE), as that can give us insight into how profitably the company is able to employ capital in its business.

First up, we’ll look at what ROCE is and how we calculate it. Second, we’ll look at its ROCE compared to similar companies. Then we’ll determine how its current liabilities are affecting its ROCE.

Understanding Return On Capital Employed (ROCE)

ROCE measures the ‘return’ (pre-tax profit) a company generates from capital employed in its business. Generally speaking a higher ROCE is better. In brief, it is a useful tool, but it is not without drawbacks. Author Edwin Whiting says to be careful when comparing the ROCE of different businesses, since ‘No two businesses are exactly alike.

So, How Do We Calculate ROCE?

The formula for calculating the return on capital employed is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets – Current Liabilities)

Or for Creative Peripherals and Distribution:

0.22 = ₹108m ÷ (₹1.3b – ₹792m) (Based on the trailing twelve months to September 2019.)

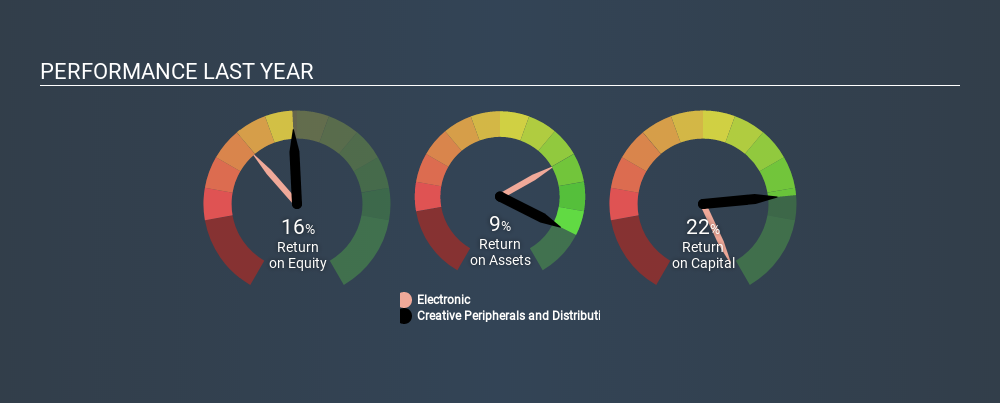

So, Creative Peripherals and Distribution has an ROCE of 22%.

See our latest analysis for Creative Peripherals and Distribution

Does Creative Peripherals and Distribution Have A Good ROCE?

One way to assess ROCE is to compare similar companies. Using our data, we find that Creative Peripherals and Distribution’s ROCE is meaningfully better than the 14% average in the Electronic industry. I think that’s good to see, since it implies the company is better than other companies at making the most of its capital. Independently of how Creative Peripherals and Distribution compares to its industry, its ROCE in absolute terms appears decent, and the company may be worthy of closer investigation.

Creative Peripherals and Distribution’s current ROCE of 22% is lower than 3 years ago, when the company reported a 41% ROCE. So investors might consider if it has had issues recently. You can see in the image below how Creative Peripherals and Distribution’s ROCE compares to its industry. Click to see more on past growth.

When considering this metric, keep in mind that it is backwards looking, and not necessarily predictive. Companies in cyclical industries can be difficult to understand using ROCE, as returns typically look high during boom times, and low during busts. ROCE is only a point-in-time measure. You can check if Creative Peripherals and Distribution has cyclical profits by looking at this free graph of past earnings, revenue and cash flow.

How Creative Peripherals and Distribution’s Current Liabilities Impact Its ROCE

Current liabilities include invoices, such as supplier payments, short-term debt, or a tax bill, that need to be paid within 12 months. Due to the way the ROCE equation works, having large bills due in the near term can make it look as though a company has less capital employed, and thus a higher ROCE than usual. To check the impact of this, we calculate if a company has high current liabilities relative to its total assets.

Creative Peripherals and Distribution has total liabilities of ₹792m and total assets of ₹1.3b. As a result, its current liabilities are equal to approximately 62% of its total assets. Creative Peripherals and Distribution’s current liabilities are fairly high, which increases its ROCE significantly.

The Bottom Line On Creative Peripherals and Distribution’s ROCE

The ROCE would not look as appealing if the company had fewer current liabilities. Creative Peripherals and Distribution shapes up well under this analysis, but it is far from the only business delivering excellent numbers . You might also want to check this free collection of companies delivering excellent earnings growth.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

[“source=simplywall”]