From Wallets and UPI to Blockchain, How Digital Payments are Evolving in India

HIGHLIGHTS The government has played a key role in the digitisation of…

Samsung Pay comes to Gear S3, use your Samsung smartwatch to make payments

Samsung has today made it possible to use the Gear S3 smartwatch with Samsung Pay, the company's…

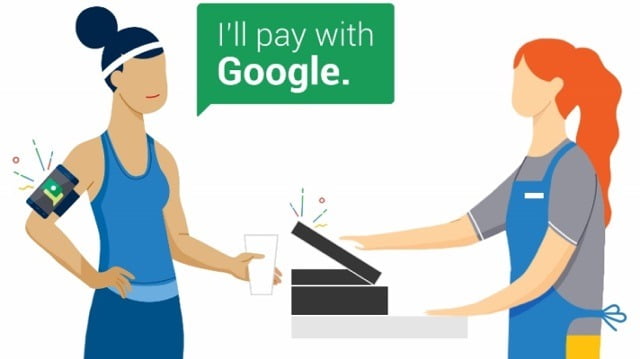

Google ends Hands Free mobile payments pilot, iOS app will stop working Feb. 8

Introduced in March for iOS and Android, Hands Free aimed to simplify…

Apple iMessage Update Lets You Send Payments, Edit Photos, More

Until very recently, the thought of Apple (NASDAQ:AAPL) ever opening its applications…